Bitcoin's Path to Global Medium of Exchange: From Dollar Dominance to Digital Currency Transition

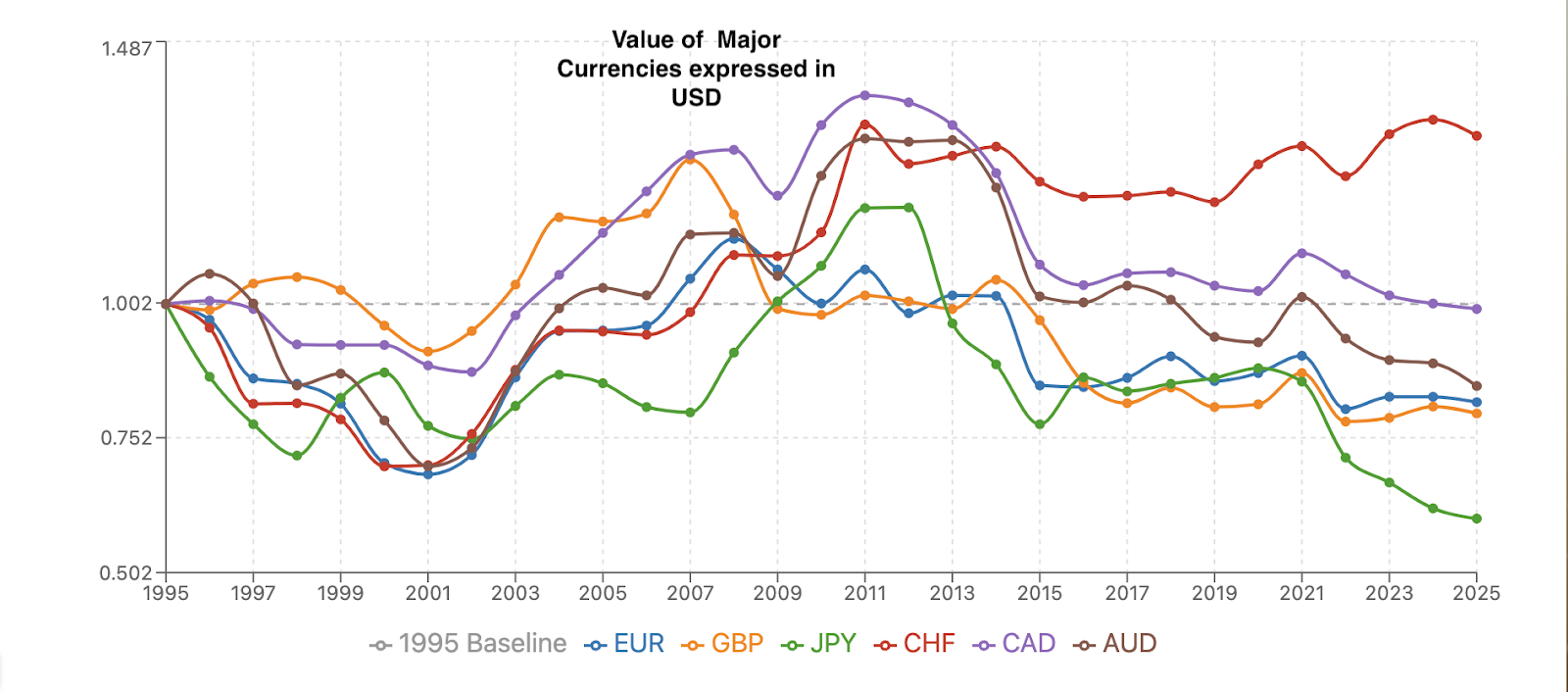

- US Dollars have long been recognized and used as the global medium of exchange, hoarded by countries such as China and Japan as foreign reserves. In nations where local currencies suffer from instability, the US dollar serves as the foundation for long-term contracts, with merchants preferring to price their goods and services in dollars rather than volatile home currencies. This preference stems from the widespread assumption that the US dollar's value would remain stable or strengthen over time. Indeed, over the past 30 years, the dollar has strengthened against most global currencies, with notable exceptions being the Chinese Yuan, Singapore Dollar, and Swiss Franc.

- However, the US government appears to be abandoning its traditional role of maintaining the dollar's global medium of exchange status. More significantly, the current administration seems intent on accumulating Bitcoin as a strategic reserve asset, with several other nations following this precedent. Beyond government initiatives, substantial private sector momentum is building, with prominent investors expressing bullish sentiment on Bitcoin's future value. Companies like MicroStrategy in the US and Metaplanet in Japan have tied their business valuations almost entirely to Bitcoin holdings. Metaplanet's stock price surge following announcements of additional Bitcoin purchases, backed by respected institutional investors, demonstrates the growing confidence in Bitcoin's long-term prospects.

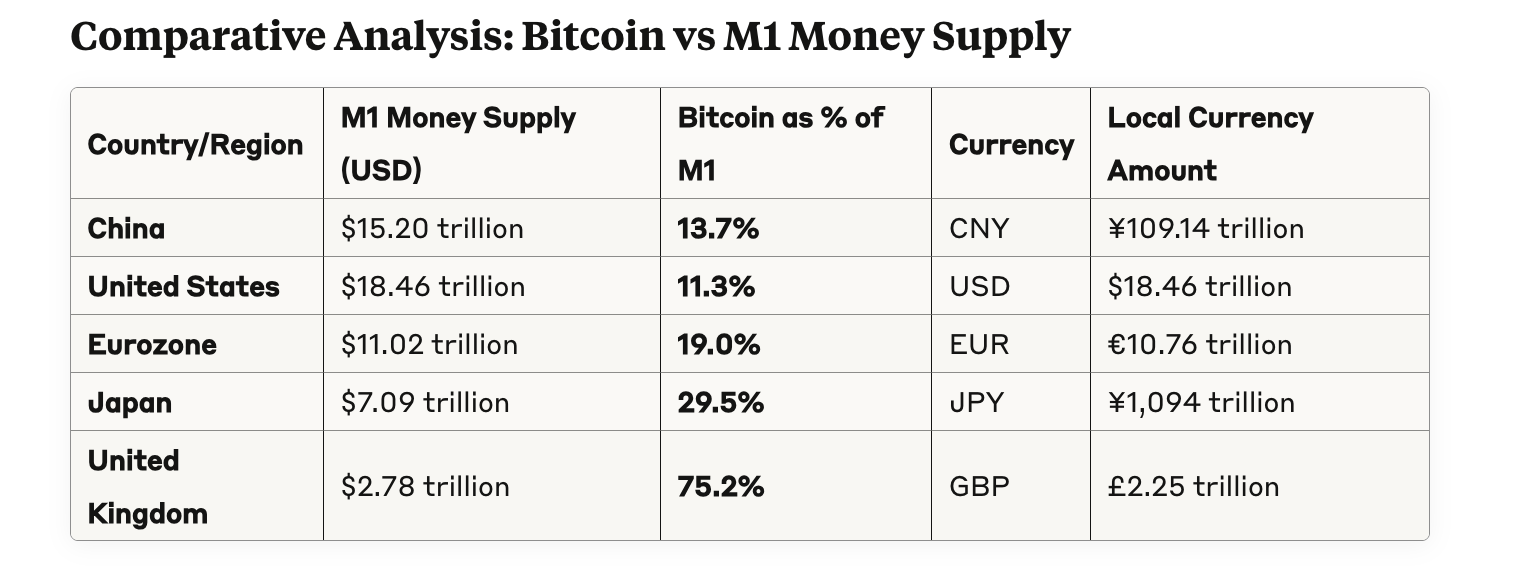

- Bitcoin's $2.093 trillion market capitalization, representing 11-17% of major economies' M1 money supplies, demonstrates it has achieved the scale necessary to potentially function as a medium of exchange, moving beyond speculative asset status to become economically significant on a global level. However, despite this impressive size, Bitcoin faces critical hurdles that must be overcome: its value remains too volatile for everyday transactions requiring predictable purchasing power, merchant acceptance infrastructure is still limited outside niche applications, and much of Bitcoin's supply is held as a store of value rather than actively circulating for commerce. While Bitcoin shows promise for specific use cases like international remittances and cross-border payments where its borderless nature provides advantages, becoming a widespread medium of exchange will require substantial additional steps including reduced price volatility, ubiquitous merchant acceptance, regulatory clarity, and improved transaction infrastructure through solutions like the Lightning Network

- Therefore, while Bitcoin's evolution into a medium of exchange is possible given its substantial scale and growing institutional backing, it remains a multi-step process requiring significant technological, regulatory, and market maturation beyond simply achieving large market capitalization. The convergence of declining dollar hegemony and rising Bitcoin adoption suggests we may be witnessing the early stages of a historic monetary transition, though the path forward requires overcoming substantial practical and technical challenges.